Homeownership can often be a rewarding experience, but for those living in high-risk areas, it can become fraught with challenges. Understanding the Top Challenges for Homeowners in High-Risk Areas and How Insurance Helps is crucial in navigating this landscape. In these regions prone to natural disasters or crime, homeowners face unique hurdles that influence their finances, safety, and overall peace of mind. Fortunately, insurance can provide a safety net, ensuring that individuals are better equipped to handle these adversities.

The Nature of High-Risk Areas

High-risk areas are defined by their vulnerability to natural disasters, such as floods, hurricanes, or wildfires, as well as other threats like high crime rates.

Geographic Vulnerability

High-risk areas often correlate with specific geographies. Coastal regions may be susceptible to hurricanes and flooding, while forested areas can be at risk of wildfires. Specific urban neighborhoods may also face higher levels of crime, making them less desirable for homeowners.

Understanding Environmental Risks

Homeowners must be aware of the environmental risks in their area. For instance, if you live near a river, understanding flood zones is crucial. Flood maps provided by agencies can help identify the likelihood of flooding in your area, allowing homeowners to take preventative measures.

Local Government Initiatives

Many local governments have initiatives aimed at helping residents mitigate these risks, including early warning systems for natural disasters and community awareness programs. Staying informed about these resources can empower homeowners to make safer choices.

Financial Implications of Living in High-Risk Areas

The financial consequences of living in these areas can be considerable. Premiums for home insurance in high-risk zones tend to be significantly higher than in lower-risk areas.

Rising Insurance Costs

Insurance companies assess risk and adjust premiums accordingly. For homeowners in high-risk areas, this translates to needing to allocate a larger portion of their budget towards insurance costs. This can lead to difficult decisions regarding coverage types, deductibles, and whether certain policies are even affordable.

Property Value Fluctuations

In high-risk areas, property values can fluctuate dramatically based on the perceived level of risk. Potential buyers may shy away from properties in these regions, affecting resale value and market stability. Homeowners may find themselves in a position where they owe more on their mortgage than their home is worth.

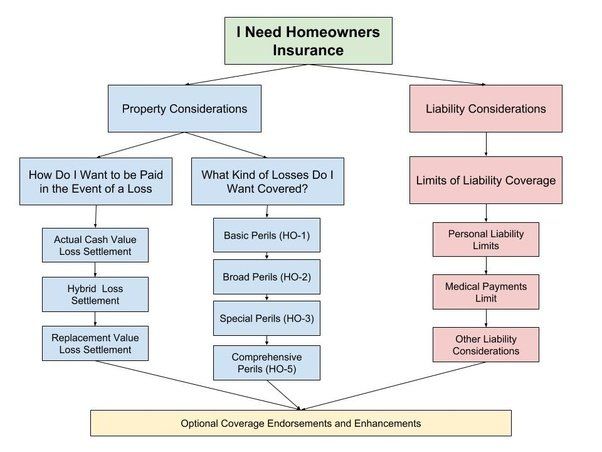

Navigating Insurance Policies

Choosing the right insurance policy requires research, understanding, and careful consideration.

Different Types of Coverage

Understanding the various types of insurance coverage available is a fundamental step for homeowners. Standard homeowner’s insurance typically covers damages caused by fire, theft, and some forms of water damage. However, residents in high-risk areas might require additional coverage options.

Flood Insurance

For homeowners in flood-prone areas, standard policies often do not cover flood damage. Obtaining separate flood insurance is essential. FEMA offers National Flood Insurance Program (NFIP) policies, which can provide critical protection for homes vulnerable to flooding.

Windstorm Insurance

In hurricane-prone regions, windstorm insurance can protect against damage caused by high winds and flying debris. Homeowners should review their current policy to ensure adequate coverage is included.

Working with Insurance Agents

Consulting with a knowledgeable insurance agent can provide homeowners with insights tailored to their specific needs.

Tailoring Your Policy

An insurance agent can assist in customizing a policy that fits the unique requirements of homeowners in high-risk areas. They can help evaluate risks, understand local regulations, and recommend the best available coverage options.

Annual Reviews

Conducting an annual review of your insurance policy with your agent is a proactive way to ensure coverage aligns with changes in risk and property value. Additionally, discussing updates to your home or improvements made can often yield discounts.

Preparing for Natural Disasters

Effective preparation can mitigate losses should disaster strike.

Creating An Emergency Plan

Developing a comprehensive emergency plan is paramount for homeowners living in high-risk areas.

Communication Strategy

Establish clear communication strategies among family members. Designate meeting points, methods of contact, and ensure all family members know the plan. This simplicity can save lives during crises.

Emergency Supplies

Stocking up on emergency supplies is another crucial element. Homeowners should prepare a disaster kit that includes food, water, first aid items, and necessary medications.

Home Hardening Techniques

Making physical changes to the property can also bolster its resiliency against natural disasters.

Reinforcement Measures

Investing in reinforcement measures—such as storm shutters, roof straps, and foundation anchors—can fortify homes against extreme weather events. These upgrades can reduce insurance premiums and enhance safety, making a compelling case for their implementation.

Landscaping Considerations

Landscaping can significantly impact how a home fares in high-risk situations. Properly positioned trees and vegetation can act as windbreaks while also minimizing flood risks. Consulting with landscaping professionals familiar with disaster preparedness can offer tailored solutions.

The Role of Community Awareness

Community plays an integral role in improving resilience against disasters.

Building Neighborhood Networks

Neighbors working together can share knowledge, resources, and support during disasters.

Organizing Local Workshops

Communities can organize workshops to educate residents about risks, emergency preparedness, and insurance implications. This shared knowledge fosters resilience and reduces individual burdens.

Establishing Local Alerts

Creating local alert systems using social media groups or community apps keeps everyone informed about potential risks, weather warnings, or safety tips.

Engaging with Local Authorities

Collaboration with local governments helps in planning effective responses to disasters.

Advocacy for Infrastructure Improvements

Communities can advocate for infrastructure improvements that lessen risks, such as improved drainage systems or stronger building codes.

Participating in Planning Meetings

Engagement in town hall meetings allows homeowners to voice concerns and stay updated on community efforts to address risks.

FAQs

What constitutes a high-risk area?

High-risk areas are locations that are vulnerable to natural disasters (floods, hurricanes, earthquakes) or high crime rates. Geographic features and historical data usually determine these categorizations.

How does living in a high-risk area affect home insurance?

Homeowners in high-risk areas typically pay higher insurance premiums due to the increased likelihood of claims. Coverage options may also be limited, requiring additional policies for specific risks.

Is flood insurance necessary if I live outside the flood zone?

While it may not be required, obtaining flood insurance is wise, as floods can occur unexpectedly. Many standard policies do not cover flood damage.

Can I lower my insurance premiums in high-risk areas?

Yes, homeowners can lower premiums through various means, such as reinforcing their homes, taking disaster preparedness courses, and bundling insurance policies with the same provider.

What steps can I take to prepare for a natural disaster?

Homeowners should create an emergency plan, stock up on emergency supplies, reinforce their homes, and stay informed about local risks and alerts.

Conclusion

Navigating the Top Challenges for Homeowners in High-Risk Areas and How Insurance Helps encompasses more than just securing adequate insurance. It involves understanding the unique risks associated with one’s geographical location, being prepared for the unexpected, and fostering community resilience. Through thorough research, strategic planning, and collaboration, homeowners can better protect their assets while also contributing to a safer living environment. Awareness and proactive measures can make all the difference in successfully managing the adversities that come with high-risk living.